Healthcare Costs 2026: Smart Financial Moves to Reduce Out-of-Pocket Expenses by 20%

The landscape of healthcare is constantly evolving, and with it, the financial burden placed upon individuals and families. As we look ahead to 2026, understanding and strategizing around rising healthcare costs becomes not just a smart move, but a necessity. The goal for many is to significantly reduce healthcare costs, specifically aiming to slash out-of-pocket expenses by a substantial margin, perhaps even 20% or more. This comprehensive guide will equip you with the knowledge and actionable strategies to navigate the complexities of the healthcare system and achieve significant savings. We’ll delve into everything from optimizing your health insurance to embracing preventive care and leveraging technology to your advantage.

The escalating trend in medical expenditures is a concern for everyone. Factors such as an aging population, advancements in medical technology, the rising cost of prescription drugs, and administrative complexities all contribute to this upward trajectory. For consumers, this often translates into higher premiums, larger deductibles, and increased co-pays, leading to considerable out-of-pocket expenses. But it’s not a battle without hope. By adopting a proactive and informed approach, you can gain greater control over your health finances and effectively reduce healthcare costs in 2026.

Understanding the Healthcare Cost Landscape in 2026

Before we can effectively reduce healthcare costs, it’s crucial to understand the forces at play. The year 2026 is projected to continue the trend of increasing healthcare expenditures. Several key drivers contribute to this:

- Inflation and Economic Factors: General economic inflation directly impacts the cost of medical services, equipment, and labor.

- Technological Advancements: While beneficial, new diagnostic tools, surgical techniques, and treatments often come with a high price tag.

- Pharmaceutical Costs: The development and marketing of new drugs, especially specialty medications, continue to be a major cost driver.

- Chronic Disease Prevalence: An increasing number of people are living with chronic conditions, requiring ongoing care and management, which accumulates significant costs over time.

- Administrative Overhead: The complex billing and administrative systems within healthcare contribute to overall expenses.

- Aging Population: As the population ages, the demand for healthcare services, particularly specialized and long-term care, naturally increases.

These factors collectively paint a picture of a challenging financial environment. However, understanding them is the first step toward devising strategies to mitigate their impact on your personal finances and effectively reduce healthcare costs.

Strategy 1: Optimize Your Health Insurance Plan

Your health insurance plan is your primary defense against exorbitant medical bills. Choosing the right plan and understanding its nuances can dramatically reduce healthcare costs and your out-of-pocket burden. This isn’t a one-size-fits-all solution; what works for one person might not work for another.

Reviewing Your Current Policy Annually

Open enrollment periods are not just a formality; they are a critical opportunity to reassess your needs. Don’t simply auto-renew. Take the time to:

- Assess Your Usage: Look back at your medical expenses from the previous year. Did you hit your deductible? How often did you visit specialists? Did you have unexpected medical events?

- Evaluate Your Health Needs: Are you expecting any major medical procedures in the coming year? Are you managing a new chronic condition? Your health needs for 2026 might be different from 2025.

- Compare Plans: Actively compare plans offered by your employer or through the marketplace. Pay close attention to premiums, deductibles, co-pays, out-of-pocket maximums, and prescription drug coverage. Sometimes, a slightly higher premium can lead to lower overall out-of-pocket costs if it comes with a lower deductible or better co-pay structure.

- Check Provider Networks: Ensure your preferred doctors, specialists, and hospitals are in-network for any new plan you consider. Out-of-network care can be significantly more expensive and often doesn’t count towards your deductible.

Understanding Different Plan Types

Various health insurance plan types offer different cost structures and levels of flexibility:

- HMOs (Health Maintenance Organizations): Typically have lower premiums and out-of-pocket costs but require you to choose a primary care physician (PCP) and get referrals for specialists.

- PPOs (Preferred Provider Organizations): Offer more flexibility in choosing providers (you don’t need a referral to see a specialist) but usually come with higher premiums and out-of-pocket costs, especially for out-of-network care.

- EPOs (Exclusive Provider Organizations): Similar to HMOs in terms of network restrictions but often don’t require a PCP referral for specialists within the network.

- POS (Point of Service) Plans: A hybrid of HMO and PPO, offering more flexibility than an HMO but with higher costs for out-of-network services.

- HDHPs (High-Deductible Health Plans) with HSAs (Health Savings Accounts): These plans have lower premiums but very high deductibles. The major benefit is the accompanying HSA, a tax-advantaged savings account for healthcare expenses. HSAs are an excellent tool to reduce healthcare costs long-term due to their triple tax advantage (contributions are tax-deductible, earnings grow tax-free, and withdrawals for qualified medical expenses are tax-free).

Consider if an HDHP with an HSA is right for you, especially if you are generally healthy and want to save for future medical expenses. The tax benefits alone can significantly reduce healthcare costs over time.

Strategy 2: Leverage Preventive Care and Wellness Programs

An ounce of prevention is worth a pound of cure, and nowhere is this more true than in healthcare. Investing in preventive care and actively participating in wellness programs can significantly reduce healthcare costs in the long run by avoiding more serious and expensive health issues.

The Power of Preventive Screenings

Most insurance plans cover a range of preventive services at no additional cost. These include:

- Annual physicals and check-ups.

- Vaccinations (flu shots, tetanus, etc.).

- Screenings for conditions like high blood pressure, cholesterol, diabetes, and certain cancers (mammograms, colonoscopies).

- Well-woman and well-child visits.

Regular screenings can detect potential health problems early when they are often easier and less expensive to treat. Neglecting these can lead to advanced conditions requiring costly interventions, thereby increasing your out-of-pocket expenses. Make it a priority to schedule and attend all recommended preventive appointments to reduce healthcare costs proactively.

Wellness Programs and Incentives

Many employers and health insurance providers offer wellness programs designed to encourage healthy living. These programs can include:

- Gym memberships or fitness class discounts.

- Smoking cessation programs.

- Weight management programs.

- Health coaching and nutritional counseling.

- Incentives for achieving health goals (e.g., lower premiums, gift cards).

Participating in these programs not only improves your overall health but can also lead to tangible financial benefits. Check with your employer or insurance provider to see what wellness benefits are available to you. These programs are designed to reduce healthcare costs for both you and the insurer by promoting a healthier populace.

Strategy 3: Be a Savvy Consumer of Medical Services

Navigating the healthcare system requires you to be an informed and proactive consumer. Asking the right questions and doing your research can uncover significant savings and help you reduce healthcare costs.

Shop Around for Procedures and Medications

Don’t assume all providers charge the same for the same service. For non-emergency procedures, imaging, and lab tests, prices can vary wildly. Use tools and resources like:

- Price Comparison Websites: Many platforms allow you to compare costs for various medical procedures in your area.

- Your Insurance Company’s Tools: Most insurers offer online tools or customer service lines to help you estimate costs for specific services with in-network providers.

- Direct Inquiries: Don’t hesitate to call different facilities (hospitals, clinics, imaging centers) and ask for their cash price or estimated cost for a procedure.

The same principle applies to prescription medications. Generic drugs are almost always significantly cheaper than their brand-name counterparts. Discuss generic alternatives with your doctor. Also, compare prices at different pharmacies, including online pharmacies, and look for discount programs (e.g., GoodRx) which can further reduce healthcare costs related to prescriptions.

Understand Your Medical Bills

Medical billing can be complex and prone to errors. Always review your medical bills thoroughly. Look for:

- Duplicate charges: Ensure you haven’t been billed twice for the same service.

- Incorrect codes: Medical billing codes (CPT codes) should accurately reflect the services you received.

- Services not rendered: Make sure you’re not being charged for services you didn’t receive.

- In-network vs. Out-of-network: Verify that all services were billed according to your in-network benefits if you stayed within your network.

If you find discrepancies, contact the provider’s billing department and your insurance company immediately. Don’t be afraid to negotiate. Hospitals and providers often have financial assistance programs or can offer discounts for prompt payment, especially if you’re paying out-of-pocket. This vigilance is key to effectively reduce healthcare costs.

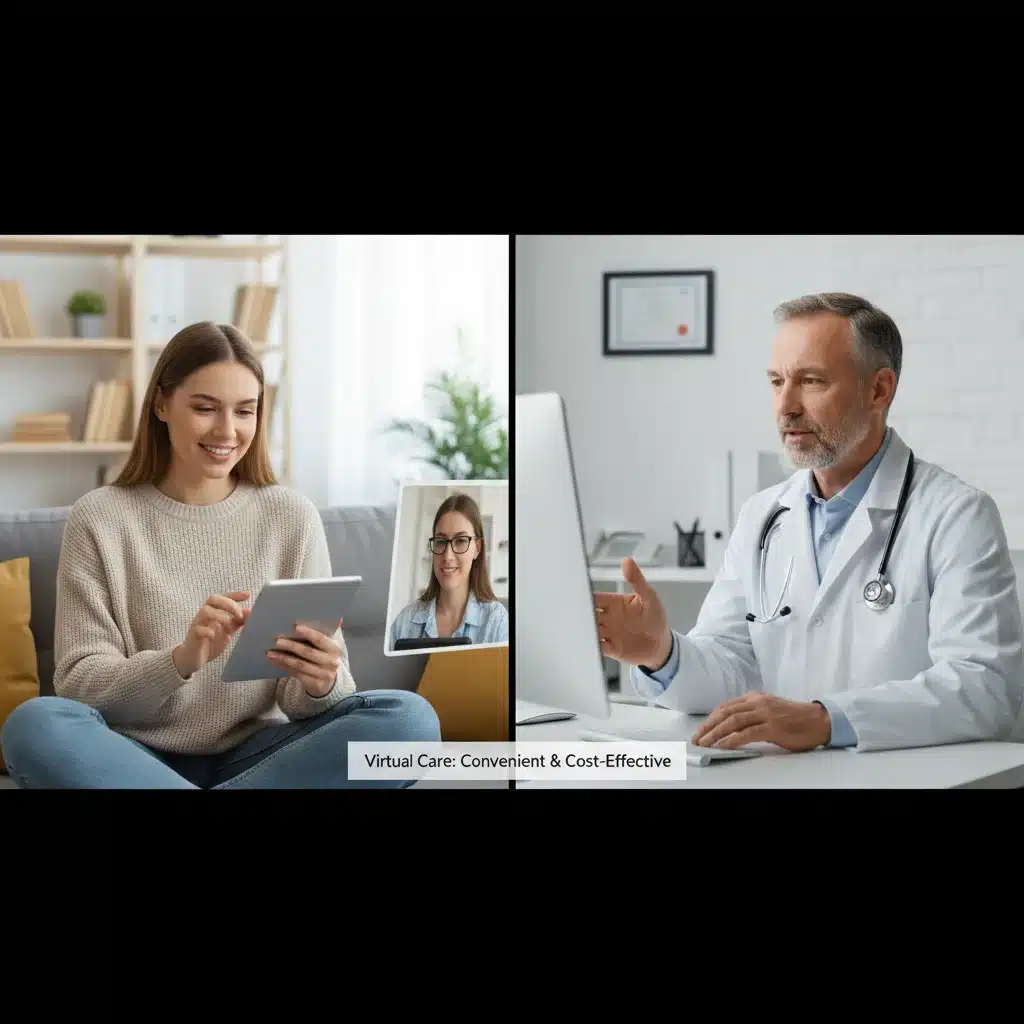

Strategy 4: Embrace Telemedicine and Virtual Care

The rise of telemedicine and virtual care has been a game-changer, offering convenience and, crucially, cost savings. This trend is only expected to grow in 2026, making it an essential tool to reduce healthcare costs.

Benefits of Telehealth

- Lower Costs: Virtual visits are often less expensive than in-person office visits, as they reduce overhead for providers and eliminate travel time and costs for patients.

- Convenience: Access care from the comfort of your home or office, saving time and reducing the need for time off work.

- Accessibility: Especially beneficial for those in rural areas or with limited access to specialists.

- Reduced Exposure: Minimizes exposure to infectious diseases in waiting rooms.

Telehealth is ideal for routine check-ups, follow-up appointments, managing chronic conditions, prescription refills, and addressing minor illnesses. Check if your insurance plan covers telemedicine services and integrate them into your healthcare routine to reduce healthcare costs.

Strategy 5: Utilize Flexible Spending Accounts (FSAs) and Health Savings Accounts (HSAs)

These tax-advantaged accounts are powerful tools for managing and reducing your out-of-pocket healthcare expenses.

Health Savings Accounts (HSAs)

As mentioned earlier, HSAs are paired with High-Deductible Health Plans (HDHPs). Their benefits are substantial:

- Tax-Deductible Contributions: Money you contribute to an HSA is pre-tax, reducing your taxable income.

- Tax-Free Growth: The money in your HSA grows tax-free, like an IRA.

- Tax-Free Withdrawals: Withdrawals for qualified medical expenses are tax-free.

- Portability: The account belongs to you, even if you change jobs or insurance plans.

- Investment Potential: After reaching a certain balance, you can often invest your HSA funds, allowing them to grow even more for future healthcare needs, including retirement healthcare.

An HSA is not just a spending account; it’s a long-term savings and investment vehicle that can significantly reduce healthcare costs over your lifetime, especially in retirement.

Flexible Spending Accounts (FSAs)

FSAs are typically offered through employers and allow you to set aside pre-tax money for qualified medical expenses. While they offer tax savings similar to an HSA for contributions and withdrawals, they have some key differences:

- “Use It or Lose It” Rule: Unlike HSAs, FSAs typically have a “use it or lose it” rule, meaning you must spend the funds by the end of the plan year (though some plans offer a grace period or allow a small rollover).

- Not Portable: You generally lose your FSA funds if you leave your employer.

- No Investment Option: FSA funds cannot be invested.

Despite the “use it or lose it” rule, an FSA can be a great way to reduce healthcare costs for predictable annual expenses like co-pays, deductibles, prescription drugs, and even over-the-counter medications and supplies. Carefully estimate your annual medical expenses to maximize the benefit without forfeiting funds.

Strategy 6: Explore Patient Assistance Programs and Discounts

Even with good insurance, some medical expenses, particularly for high-cost prescription drugs, can be daunting. Thankfully, various programs exist to help.

Pharmaceutical Patient Assistance Programs

Many pharmaceutical companies offer programs to help patients afford their medications. These programs often provide free or low-cost drugs to eligible individuals, especially those with low incomes or inadequate insurance coverage. Your doctor’s office or the drug manufacturer’s website are good starting points to find these programs.

Hospital Financial Assistance Programs

Most hospitals have policies to assist patients who cannot afford their medical bills. These programs, often called “charity care,” can provide full or partial waivers of bills based on income and other factors. Don’t hesitate to ask the hospital’s billing department about their financial assistance options, especially for large, unexpected medical expenses. Many hospitals are legally required to have such programs.

Non-Profit Organizations

Numerous non-profit organizations are dedicated to helping patients with specific diseases or conditions cover their medical costs. These organizations might offer grants, co-pay assistance, or help with travel expenses for treatment. A quick online search for your specific condition and “patient assistance” can yield valuable resources to reduce healthcare costs.

Strategy 7: Advocate for Yourself and Negotiate

The healthcare system can feel intimidating, but remember that you have the right to ask questions and negotiate. Being your own advocate can lead to significant savings.

Negotiating Medical Bills

If you receive a bill that seems too high, or if you’re uninsured, don’t just pay it. Call the billing department and try to negotiate. Here are some tips:

- Ask for an Itemized Bill: Request a detailed, itemized bill to understand every charge.

- Question Charges: If you see something you don’t understand or believe is incorrect, ask for clarification.

- Offer a Lump Sum Payment: Many providers will offer a discount (e.g., 10-30%) for immediate payment of the full balance.

- Set Up a Payment Plan: If you can’t pay in a lump sum, negotiate a manageable payment plan without interest.

- Highlight Financial Hardship: If you’re facing financial difficulties, explain your situation. Providers may be more willing to work with you.

This negotiation can be a powerful way to directly reduce healthcare costs that have already been incurred.

Understanding Your Rights

Familiarize yourself with laws like the No Surprises Act, which protects consumers from unexpected medical bills from out-of-network providers in emergency situations or for certain non-emergency services at in-network facilities. Knowing your rights empowers you to challenge unfair billing practices and reduce healthcare costs.

Strategy 8: Prioritize Mental Health Care

Mental health is an integral part of overall well-being, and neglecting it can lead to physical health problems and increased medical expenses. Prioritizing mental health care can indirectly reduce healthcare costs.

Integrating Mental and Physical Health

Seek out providers who offer integrated care, where mental health professionals work alongside primary care physicians. This holistic approach can lead to better overall health outcomes and prevent more serious, costly interventions down the line. Many insurance plans are now required to cover mental health services at the same level as physical health services, so make sure to check your benefits.

Low-Cost and Free Mental Health Resources

If cost is a barrier, explore options like:

- Community Mental Health Centers: Often offer services on a sliding scale.

- University Clinics: Provide affordable therapy and counseling from supervised students.

- Support Groups: Many are free and offer valuable peer support.

- Mental Health Apps and Online Resources: While not a substitute for professional help, many apps offer tools for managing stress, anxiety, and depression.

Addressing mental health proactively is a vital component in the broader effort to reduce healthcare costs by maintaining overall health.

Strategy 9: Embrace Technology for Health Management

Technology offers a plethora of tools that can help you manage your health more effectively and, consequently, reduce healthcare costs.

Wearable Devices and Health Apps

Smartwatches and fitness trackers can monitor vital signs, track activity levels, and remind you to take medications. Health apps can help you manage chronic conditions, track symptoms, and even connect you with health coaches. By staying on top of your health, you can often prevent conditions from worsening, which leads to fewer doctor visits and lower expenses.

Online Patient Portals

Most healthcare providers offer online patient portals where you can:

- Access your medical records and test results.

- Communicate with your care team.

- Schedule appointments.

- Request prescription refills.

These portals empower you to be an active participant in your care, ensuring you have all the information you need to make informed decisions and manage your health efficiently, contributing to your ability to reduce healthcare costs.

Putting It All Together: Your 20% Reduction Plan

Achieving a 20% reduction in out-of-pocket healthcare costs by 2026 is an ambitious but attainable goal. It requires a multi-faceted approach and consistent effort. Here’s a brief recap of how to integrate these strategies:

- Annual Insurance Audit: Dedicate time during open enrollment to thoroughly review and compare health insurance plans. Consider HDHPs with HSAs if appropriate.

- Prioritize Prevention: Schedule all recommended preventive screenings and actively participate in wellness programs offered by your employer or insurer.

- Be a Smart Consumer: Shop around for non-emergency services, compare prescription drug prices, and always review your medical bills for accuracy.

- Utilize Telehealth: Opt for virtual visits when appropriate for convenience and cost savings.

- Maximize Tax-Advantaged Accounts: Contribute generously to your HSA or FSA to leverage tax benefits for healthcare expenses.

- Seek Assistance: Don’t hesitate to explore patient assistance programs for medications or hospital financial aid for large bills.

- Advocate and Negotiate: Question charges, negotiate bills, and understand your patient rights.

- Holistic Health: Invest in mental health care as a crucial component of overall well-being, preventing more complex and costly issues.

- Embrace Health Tech: Use apps and wearables to proactively manage your health and stay informed.

By implementing these strategies systematically, you’re not just reacting to rising healthcare costs; you’re proactively shaping your financial future and taking control of your health. The journey to reduce healthcare costs by 20% in 2026 starts with informed decisions and consistent action.

The Future of Healthcare Costs and Your Role

The trajectory of healthcare costs will likely continue its upward trend, driven by innovation, demographic shifts, and economic pressures. However, the individual’s role in managing these costs is becoming increasingly significant. Empowering yourself with knowledge, being proactive in your health management, and making informed financial decisions are no longer optional but essential skills for navigating the modern healthcare system.

Beyond personal financial savings, collectively, informed consumers can also drive change. As more individuals demand transparency in pricing, question billing practices, and choose cost-effective care options, the healthcare industry will be incentivized to respond with more accessible and affordable solutions. Your efforts to reduce healthcare costs not only benefit your wallet but also contribute to a broader movement towards a more efficient and equitable healthcare system.

Remember, achieving a 20% reduction in out-of-pocket expenses is a significant accomplishment that requires diligence. Start small, implement one strategy at a time, and gradually build a robust financial health plan. Regularly reassess your progress, adapt your strategies as your needs change, and stay informed about new opportunities to save. The path to reducing healthcare costs is continuous, but with these tools, you are well-equipped for success in 2026 and beyond.