ACA Subsidies 2026: How Policy Extensions Can Reduce Your Premiums by Up to 15%

The landscape of healthcare affordability in the United States is constantly evolving, with policy decisions often having a profound and direct impact on the wallets of millions of Americans. One of the most significant aspects of the Affordable Care Act (ACA) has been its provision for subsidies, designed to make health insurance more accessible and affordable for individuals and families. As we look towards 2026, crucial policy extensions are set to continue these vital financial supports, potentially reducing your health insurance premiums by as much as 15%.

Understanding these extensions, their implications, and how to maximize their benefits is paramount for anyone navigating the complex world of health insurance. This comprehensive guide will delve into the specifics of ACA Subsidies 2026, exploring the mechanisms behind these savings, who is eligible, and what steps you can take to ensure you are receiving the maximum possible financial assistance. We will also examine the broader context of these policy decisions, their historical roots, and their projected future impact on the American healthcare system.

The Foundation of ACA Subsidies: A Brief Overview

To truly appreciate the significance of the ACA Subsidies 2026 extensions, it’s helpful to first understand the foundational principles of the Affordable Care Act’s financial assistance programs. Signed into law in 2010, the ACA aimed to expand health insurance coverage, improve health outcomes, and reduce healthcare costs. A cornerstone of this effort was the introduction of premium tax credits (subsidies) and cost-sharing reductions (CSRs).

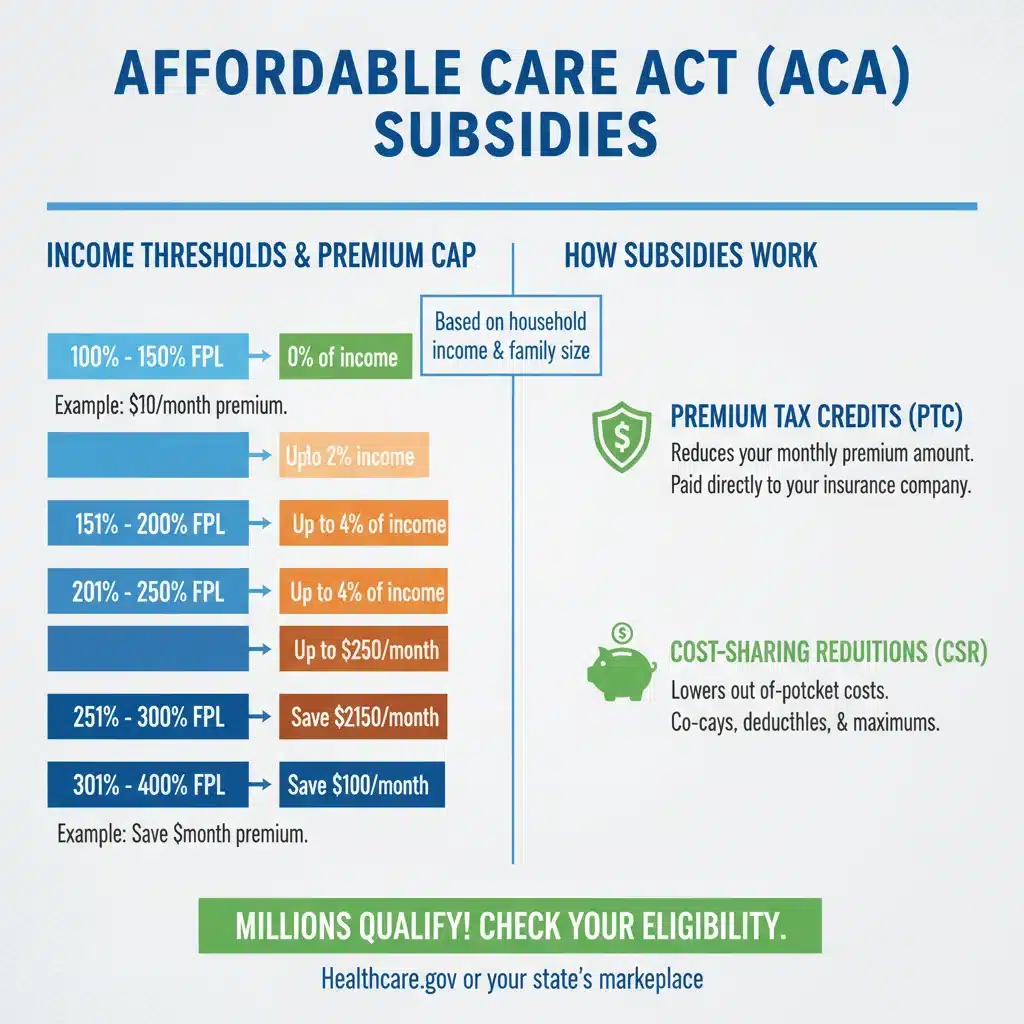

Premium tax credits are designed to lower the monthly amount you pay for health insurance premiums purchased through the Health Insurance Marketplace. These credits are based on a sliding scale, meaning that individuals and families with lower incomes receive more financial assistance. The original ACA legislation set specific income thresholds, capping the percentage of household income that individuals would have to pay for a benchmark silver plan.

Cost-sharing reductions, on the other hand, help reduce the amount you have to pay out-of-pocket for deductibles, co-payments, and co-insurance. These are only available if you enroll in a silver plan and meet certain income criteria.

The goal of these subsidies was clear: to ensure that health insurance was not only available but also genuinely affordable, preventing individuals from being priced out of essential healthcare coverage. Over the years, the effectiveness and scope of these subsidies have been subject to legislative changes and adjustments, culminating in the current discussions around the ACA Subsidies 2026 extensions.

The American Rescue Plan Act and Enhanced Subsidies

A pivotal moment in the evolution of ACA subsidies came with the passage of the American Rescue Plan Act (ARPA) in March 2021. This legislation significantly enhanced ACA subsidies, making them more generous and expanding eligibility to a broader range of income levels. Prior to ARPA, individuals with incomes above 400% of the federal poverty level (FPL) were generally ineligible for premium tax credits. ARPA eliminated this income cap, ensuring that no one would have to pay more than 8.5% of their household income for a benchmark silver plan, regardless of their income.

Furthermore, ARPA also increased the amount of financial assistance for those who were already eligible for subsidies. This meant lower monthly premiums for millions of Americans, with many seeing their premiums reduced to zero or a very low amount. These enhanced subsidies were initially set to expire at the end of 2022, raising concerns about a significant increase in healthcare costs for many households.

The Inflation Reduction Act: Extending the Lifeline to 2025

Recognizing the critical role of ARPA’s enhanced subsidies in maintaining healthcare affordability, Congress passed the Inflation Reduction Act (IRA) in August 2022. A key provision of the IRA was the extension of these enhanced ACA subsidies for an additional three years, through the end of 2025. This legislative action provided much-needed stability and continued relief for millions of Americans who rely on these subsidies to afford their health insurance.

The extension through 2025 was a welcome development, preventing a ‘subsidy cliff’ that would have led to substantial premium increases for many. It underscored a commitment to ensuring ongoing access to affordable healthcare, even as economic pressures continued to impact households across the nation. However, the question of what would happen beyond 2025 remained, setting the stage for the current discussions surrounding ACA Subsidies 2026.

Understanding the 2026 Policy Extensions: What’s on the Table?

As the expiration of the Inflation Reduction Act’s subsidy extensions looms at the end of 2025, policymakers are actively discussing further extensions to prevent a sudden surge in healthcare costs. The primary goal of these proposed ACA Subsidies 2026 extensions is to continue the enhanced financial assistance that has been in place since ARPA. This would mean maintaining the current framework where:

- No Income Cap: Individuals and families with incomes above 400% FPL would continue to be eligible for subsidies, ensuring that no one pays more than 8.5% of their income for a benchmark silver plan.

- Increased Subsidy Amounts: Those with lower incomes would continue to receive more generous subsidies, potentially leading to very low or even $0 premiums for many.

- Expanded Eligibility: More people would find themselves eligible for financial help, drawing more individuals into the Marketplace and expanding overall coverage.

The ongoing debates center on the duration and scope of these extensions. While a permanent extension would provide maximum stability, short-term extensions are often more politically feasible. Regardless of the exact legislative outcome, the intention is to avoid a situation where millions of Americans face significant premium hikes, which could lead to a decrease in health insurance coverage and an increase in uninsured rates.

How These Extensions Can Reduce Your Premiums by Up to 15%

The continuation of the enhanced ACA Subsidies 2026 framework is projected to have a substantial impact on individual and family premiums. The ‘up to 15%’ reduction is not a universal figure but rather a potential outcome for specific income brackets and geographic locations. Here’s how these savings are realized:

- Maintaining the 8.5% Income Cap: For individuals and families earning above 400% FPL, the elimination of the income cap and the 8.5% premium contribution limit are critical. Without these enhanced subsidies, their premiums could skyrocket to pre-ARPA levels, which could represent a 10-15% increase or even more, depending on their income and the cost of benchmark plans in their area. By extending these provisions, their premiums remain capped, effectively ‘reducing’ what they would otherwise have to pay.

- Increased Subsidy Amounts for Lower Incomes: For those below 400% FPL, the enhanced subsidies mean a larger portion of their premium is covered by the government. This translates directly into lower out-of-pocket costs. While the percentage reduction might be different for each income level, the overall effect is a significant decrease in the net premium paid. For some, this could mean a reduction of 15% or even higher compared to what they would pay without the enhanced subsidies.

- Offsetting Inflationary Pressures: Healthcare costs, like many other sectors, are subject to inflation. Without enhanced subsidies, annual premium increases could be absorbed entirely by consumers. The extended subsidies help cushion this blow, effectively reducing the net premium increase that individuals would experience due to market forces.

It’s important to note that the exact percentage of savings will vary based on several factors, including your household income, family size, the cost of health plans in your specific rating area, and the specific plan you choose. However, the overarching effect of extending these policies is a continuation of significant financial relief for millions.

Who Benefits Most from ACA Subsidies 2026?

While the ACA Subsidies 2026 extensions are designed to benefit a broad spectrum of individuals and families, certain groups stand to gain the most:

- Middle-Income Households: Previously, individuals and families with incomes just above 400% FPL were often hit hardest by the absence of subsidies. The extension of the no-income-cap rule ensures that these households continue to receive crucial financial assistance, preventing them from paying a disproportionately high percentage of their income for healthcare.

- Low-Income Individuals and Families: Those at the lower end of the income spectrum will continue to benefit from the most generous subsidies, often resulting in very affordable or even free premiums. These extensions are vital for maintaining their access to essential health services.

- Self-Employed Individuals and Small Business Owners: These groups often rely heavily on the Health Insurance Marketplace for coverage, as they may not have access to employer-sponsored plans. The continued availability of robust subsidies is critical for their financial well-being and ability to secure health insurance.

- Individuals Facing Unemployment or Income Fluctuations: The ACA’s design, with subsidies adjusting to income changes, provides a safety net for those experiencing job loss or variable income. The extensions ensure this safety net remains robust.

Essentially, anyone purchasing health insurance through the Health Insurance Marketplace who meets the income criteria will continue to see benefit from these extended policies, making healthcare more attainable and less burdensome financially.

Navigating Eligibility for ACA Subsidies 2026

Eligibility for ACA Subsidies 2026 will largely mirror the current criteria, primarily based on your household income relative to the Federal Poverty Level (FPL) and whether you have access to other affordable health coverage. Here’s a breakdown:

Income Thresholds

Your Modified Adjusted Gross Income (MAGI) is the key factor. For premium tax credits, your MAGI generally needs to be between 100% and 400% of the FPL. However, with the extended enhanced subsidies, the ‘cliff’ at 400% FPL is removed, meaning even if your income is above this, you could still qualify if your premium contribution would exceed 8.5% of your income.

- Below 100% FPL: In states that have expanded Medicaid, individuals below 138% FPL typically qualify for Medicaid. In non-expansion states, individuals below 100% FPL may fall into a ‘coverage gap’ where they don’t qualify for Medicaid or ACA subsidies.

- 100% – 150% FPL: You may qualify for very generous subsidies, potentially leading to $0 monthly premiums for benchmark plans.

- 150% – 250% FPL: Significant subsidies are available to keep your premium contribution low.

- 250% – 400% FPL: Subsidies are available on a sliding scale, reducing your premium burden.

- Above 400% FPL: With the extended enhanced subsidies, you qualify if your premium for the benchmark plan would be more than 8.5% of your household income.

It’s crucial to report accurate income information when applying through the Marketplace, as subsidies are reconciled against your actual income when you file your federal tax return.

No Access to Affordable Employer-Sponsored Coverage

You generally won’t qualify for ACA subsidies if you have access to affordable health insurance through an employer (either your own or a family member’s). Employer-sponsored coverage is considered ‘affordable’ if the employee’s share of the premium for self-only coverage is less than a certain percentage of their household income (this percentage is adjusted annually).

No Access to Government Programs

You also won’t qualify for subsidies if you are eligible for other government-sponsored programs like Medicare, Medicaid, or CHIP (Children’s Health Insurance Program).

The application process for ACA Subsidies 2026 will continue to be through HealthCare.gov or your state’s marketplace website. These platforms are designed to guide you through eligibility determination and plan selection.

The Economic and Social Impact of Continued Subsidies

The decision to extend ACA Subsidies 2026 goes beyond individual financial relief; it has significant broader economic and social implications:

- Reduced Uninsured Rates: By making health insurance more affordable, subsidies encourage more people to enroll, leading to lower uninsured rates and a healthier population overall.

- Improved Public Health: When more people have insurance, they are more likely to seek preventive care, manage chronic conditions, and receive timely treatment, leading to better public health outcomes and reduced reliance on emergency room visits for primary care.

- Financial Stability for Families: Healthcare costs are a leading cause of bankruptcy in the U.S. Subsidies protect families from catastrophic medical bills, contributing to greater financial stability.

- Economic Stimulus: Lower healthcare costs free up household income for other spending, potentially stimulating local economies.

- Stability for the Insurance Market: A larger, healthier risk pool fostered by increased enrollment can help stabilize insurance markets, potentially leading to more competitive plans and broader choices.

These extensions are not merely a temporary fix but represent a continued investment in the health and economic security of the American populace.

Preparing for Open Enrollment: Maximizing Your Savings

Even with the promise of continued ACA Subsidies 2026, proactive planning during open enrollment is crucial to maximize your savings and ensure you have the best possible coverage. Here are steps you can take:

- Review Your Current Plan: Don’t automatically re-enroll. Your health needs might have changed, and new plans or different subsidy levels could make another option more affordable or better suited.

- Update Your Income Information: Your subsidy amount is directly tied to your estimated household income for the upcoming year. If your income has changed or you anticipate a change, update this information accurately to avoid overpayment or underpayment of subsidies.

- Compare All Available Plans: Even if you like your current plan, compare it against all other options available in your metal tier (Bronze, Silver, Gold, Platinum) and even across tiers. Premiums, deductibles, co-pays, and out-of-pocket maximums can vary significantly.

- Consider Silver Plans for CSRs: If your income is below 250% FPL, enrolling in a Silver plan makes you eligible for Cost-Sharing Reductions (CSRs), which can significantly lower your deductibles, co-pays, and out-of-pocket maximums. These are separate from premium tax credits but equally valuable.

- Seek Assistance: If you find the process overwhelming, utilize the free resources available. HealthCare.gov provides navigators and certified assisters who can help you understand your options, determine eligibility, and enroll in a plan.

- Be Aware of Deadlines: Open enrollment periods are strict. Missing the deadline could mean you can’t get coverage until the next year, unless you qualify for a Special Enrollment Period due to a life event (like marriage, birth of a child, or loss of other coverage).

By taking these steps, you can ensure that you are fully leveraging the benefits of ACA Subsidies 2026 and securing comprehensive, affordable health insurance.

The Future Outlook: Beyond 2026

While the focus is currently on the ACA Subsidies 2026 extensions, the long-term future of these financial aids remains a topic of ongoing discussion and potential legislative action. Healthcare policy is dynamic, and future Congresses and administrations may revisit the structure and funding of these subsidies.

Advocates for permanent extensions argue that healthcare affordability should not be subject to recurring legislative battles. They point to the proven track record of subsidies in reducing uninsured rates and improving access to care. Opponents often raise concerns about the cost to taxpayers and explore alternative approaches to healthcare reform.

Regardless of the political landscape, the debate over healthcare affordability will undoubtedly continue. For consumers, staying informed about policy changes and understanding how they impact your personal situation will be key. The experience with ARPA and IRA demonstrates a willingness to prioritize healthcare access, offering hope that robust financial assistance will remain a cornerstone of the American healthcare system for the foreseeable future.

Conclusion: Securing Your Healthcare with ACA Subsidies 2026

The potential extension of ACA Subsidies 2026 is a critical development for millions of Americans seeking affordable health insurance. These policy decisions underscore a continued commitment to making healthcare accessible by significantly reducing premium costs, potentially by up to 15% or more for eligible individuals and families. By understanding how these subsidies work, who qualifies, and how to navigate the enrollment process, you can ensure that you are taking full advantage of the financial assistance available.

As open enrollment approaches, empower yourself with knowledge and prepare to make informed decisions about your health coverage. The extended subsidies offer a powerful tool in your financial planning, helping to safeguard your health and your wallet in the years to come. Stay vigilant, stay informed, and secure the affordable healthcare you deserve.