Federal Housing Initiatives 2026: Mortgage Savings Up To 10%

New federal housing initiatives for 2026 are poised to offer significant financial relief, potentially saving American families up to 10% on their mortgage costs through various programs and incentives designed to enhance home affordability.

Are you dreaming of owning a home, or perhaps looking to refinance your current mortgage? The landscape of homeownership in the United States is on the brink of a significant shift. Breaking: New Federal Housing Initiatives for 2026 Could Save Families Up To 10% on Mortgage Costs, offering a beacon of hope for millions of American families grappling with rising housing expenses. These forthcoming programs are designed to make homeownership more accessible and affordable than ever before.

Understanding the New Federal Housing Initiatives for 2026

The federal government is preparing to roll out a comprehensive suite of housing initiatives in 2026, targeting various segments of the housing market. These programs are not merely incremental adjustments; they represent a concerted effort to address the long-standing challenges of housing affordability and access. The primary goal is to alleviate the financial burden on families, making the dream of homeownership a tangible reality for more Americans.

These initiatives are expected to encompass a range of strategies, from direct financial assistance to regulatory reforms designed to streamline the mortgage process. Understanding the scope and intent behind these programs is crucial for families and individuals looking to benefit. It’s about more than just saving money; it’s about fostering greater financial stability and community development across the nation.

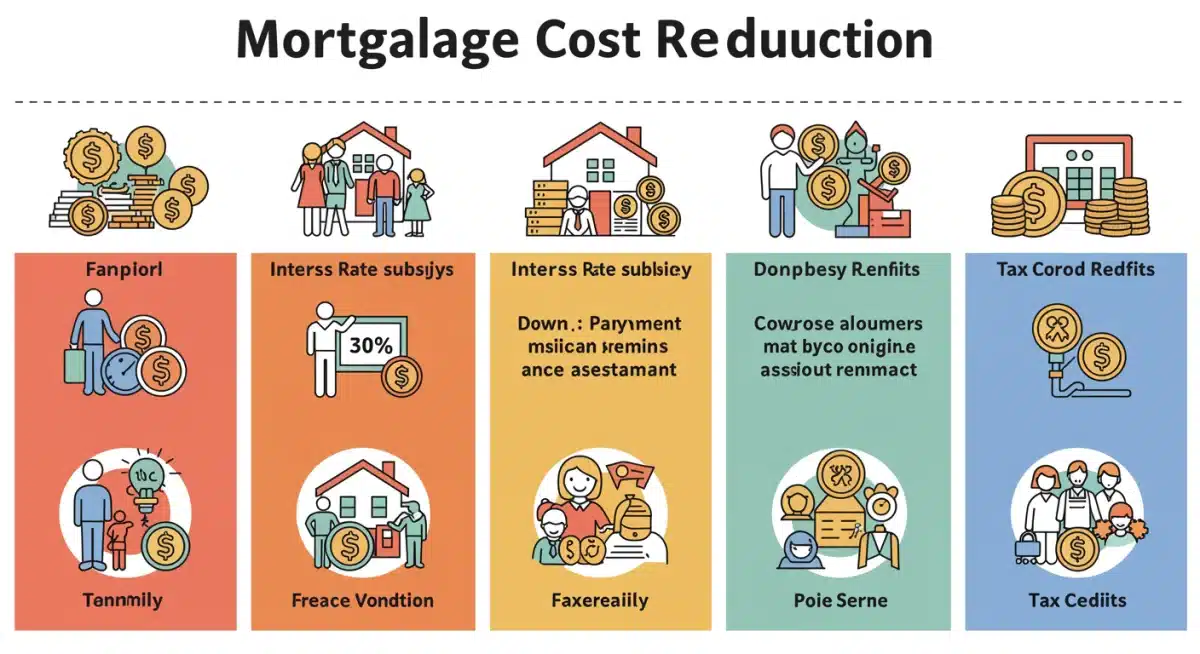

Key Pillars of the 2026 Housing Plan

- Down Payment Assistance Programs: Enhanced federal grants and loans to help first-time homebuyers overcome the initial hurdle of a substantial down payment.

- Interest Rate Subsidies: Targeted subsidies designed to lower effective interest rates for eligible borrowers, reducing monthly mortgage payments.

- Tax Credits for Homeowners: New or expanded tax credits aimed at offsetting various homeownership costs, including property taxes and mortgage interest.

- Streamlined Refinancing Options: Simplified processes and reduced fees for existing homeowners to refinance their mortgages at more favorable terms.

The blend of direct financial aid and regulatory adjustments aims to create a more equitable and accessible housing market. These pillars are interconnected, working in synergy to provide a robust framework for supporting aspiring and current homeowners. The anticipation surrounding these initiatives is high, as they promise to bring tangible relief to household budgets.

Ultimately, this section highlights the foundational elements of the upcoming federal housing initiatives. By understanding these core components, families can begin to assess how these changes might impact their financial planning and homeownership aspirations. The focus remains on making housing more affordable and sustainable for a broader demographic.

Potential Mortgage Savings: How Families Could Save Up To 10%

The headline promise of saving up to 10% on mortgage costs is a significant motivator for many families. This percentage isn’t arbitrary; it reflects the cumulative impact of various programs designed to reduce both upfront and ongoing housing expenses. Achieving such savings could translate into hundreds, or even thousands, of dollars annually, significantly easing financial pressures.

These savings can materialize in several ways. For new homebuyers, reduced down payments mean lower initial out-of-pocket expenses and potentially smaller loan amounts. For all homeowners, lower interest rates or effective interest rates through subsidies directly translate to smaller monthly payments. Furthermore, tax credits can provide a welcome boost during tax season, effectively reducing the overall cost of homeownership.

Breaking Down the 10% Savings Potential

- Reduced Interest Payments: Federal subsidies could lower your interest rate by 0.5% to 1.0%, leading to substantial savings over the life of a loan.

- Lower Private Mortgage Insurance (PMI): Enhanced down payment assistance may help borrowers reach the 20% equity threshold faster, eliminating PMI costs.

- Direct Financial Assistance: Grants for down payments or closing costs directly reduce the principal amount financed, decreasing overall mortgage obligations.

- Tax Benefits: Expanded deductions or credits for mortgage interest and property taxes can further reduce the net cost of homeownership.

The combination of these financial mechanisms is what makes the 10% savings target achievable for many. It’s not about a single magical program but rather a strategic layering of benefits that address different cost centers of homeownership. This holistic approach aims to provide comprehensive relief.

In essence, the potential for significant mortgage savings in 2026 is rooted in a multi-faceted approach by the federal government. Families should actively explore each component to understand how they can maximize their benefits and achieve the promised cost reductions. This could be a game-changer for household budgets.

Eligibility Requirements and Application Process

To ensure these new federal housing initiatives for 2026 reach those who need them most, specific eligibility criteria will be established. While the full details are still being finalized, general guidelines are expected to focus on income levels, first-time homebuyer status, and potentially geographic location. Understanding these requirements early will be crucial for prospective applicants.

The application process is also anticipated to be streamlined, leveraging technology to make it more accessible and less cumbersome. Federal agencies are reportedly working on integrated platforms that could simplify documentation submission and program matching, reducing the administrative burden on applicants. This user-friendly approach is a key component of the initiative’s success.

Anticipated Eligibility Criteria

While exact figures will vary, common criteria are likely to include:

- Income Limitations: Programs will likely target low-to-moderate income families, with regional adjustments for cost of living.

- First-Time Homebuyer Status: Many initiatives will prioritize individuals or families who have not owned a home in the past three years.

- Credit Score Requirements: While some programs may offer flexibility, a reasonable credit score will generally be beneficial.

- Homebuyer Education: Participation in approved homebuyer education courses might be a prerequisite for certain benefits.

The application process will likely involve working with approved lenders and housing counselors. These professionals can guide applicants through the necessary paperwork, ensure eligibility, and help maximize the benefits received. Proactive engagement with these resources will be vital for a successful application.

Preparing for the application process now, even before specific details are released, can give families a significant advantage. Gathering financial documents, checking credit scores, and attending pre-purchase counseling can set the stage for a smooth application once the programs launch. This section emphasizes the importance of readiness and understanding the anticipated prerequisites.

Impact on the Housing Market and Economy

The introduction of such substantial new federal housing initiatives for 2026 is expected to have a ripple effect across the entire housing market and broader economy. By increasing affordability and access to homeownership, these programs could stimulate demand, influence property values, and contribute to overall economic growth. The implications extend beyond individual households.

A healthier housing market often correlates with a stronger economy. Increased home sales can boost related industries, such as construction, real estate services, and home improvement. Moreover, greater homeownership can foster community stability and wealth creation for families, leading to increased consumer spending and investment.

Economic Ramifications of Enhanced Homeownership

The anticipated impacts are multifaceted:

- Increased Demand: More eligible buyers could lead to a modest increase in housing demand, particularly in affordable segments.

- Stabilized Property Values: While increasing demand, the programs also aim to prevent runaway price inflation by potentially increasing supply through incentives for builders.

- Job Creation: A stimulated housing sector supports jobs in construction, real estate, lending, and related services.

- Wealth Creation: Homeownership remains a primary driver of household wealth, contributing to long-term financial security for families.

However, policymakers will need to carefully monitor the market to ensure these initiatives don’t inadvertently create new challenges, such as overheating certain regional markets. The goal is sustainable growth and equitable access, not speculative bubbles. Balancing these factors will be key to the long-term success of the programs.

In summary, the 2026 federal housing initiatives are poised to be a significant economic catalyst. Their potential to boost homeownership and stabilize the housing market could lead to widespread benefits, from individual family finances to national economic indicators. This underscores the far-reaching importance of these upcoming changes.

Preparing for the 2026 Initiatives: A Guide for Families

With the new federal housing initiatives for 2026 on the horizon, proactive preparation is the best strategy for families looking to capitalize on these opportunities. Waiting until the last minute could mean missing out on crucial benefits or facing delays in the application process. A well-thought-out plan can make all the difference.

Preparation involves several key steps, from financial housekeeping to understanding market trends. It’s about positioning yourself to be an ideal candidate for the programs, ensuring you meet eligibility criteria and can move quickly once the initiatives are officially launched. This foresight can save considerable time and stress.

Steps to Take Now

Consider these actions to prepare:

- Assess Your Financial Health: Review your credit score, debt-to-income ratio, and savings. Work to improve any areas that might hinder eligibility.

- Save for a Down Payment: Even with assistance, having some personal savings for a down payment or closing costs can strengthen your application.

- Research Local Housing Markets: Understand the housing inventory and price trends in your target areas.

- Attend Homebuyer Education: Many non-profit organizations offer free or low-cost homebuyer education courses that can be invaluable.

Engaging with a trusted financial advisor or housing counselor can also provide personalized guidance. These professionals can offer insights into your specific situation and help you navigate the complexities of preparing for new federal programs. Their expertise can be a valuable asset in your homeownership journey.

Ultimately, being prepared means being informed and financially ready. By taking these preparatory steps, families can significantly enhance their chances of benefiting from the 2026 federal housing initiatives, turning potential savings into actual financial relief and a more secure future in their own home.

Long-Term Benefits and Sustainable Homeownership

The vision behind the new federal housing initiatives for 2026 extends beyond immediate mortgage savings; it aims to foster long-term benefits and sustainable homeownership. These programs are designed not just to get people into homes, but to help them stay there, building equity and contributing to their financial well-being over decades. It’s an investment in the future stability of American families.

Sustainable homeownership involves more than just affordable monthly payments. It encompasses access to resources for home maintenance, protection against predatory lending, and pathways to build wealth through property appreciation. The initiatives are expected to include components that address these broader aspects of homeownership, creating a more resilient system.

Building Equity and Financial Security

The long-term advantages are substantial:

- Wealth Accumulation: Home equity is a primary source of wealth for many families, providing a financial safety net and asset for future generations.

- Community Stability: Higher rates of sustainable homeownership often lead to more stable communities, with residents invested in local schools and services.

- Reduced Financial Stress: Predictable and affordable housing costs reduce overall financial stress, allowing families to invest in other areas of their lives.

- Access to Future Opportunities: Home equity can be leveraged for education, business ventures, or retirement planning, opening new financial doors.

The focus on sustainability also means integrating environmental considerations where possible, promoting energy-efficient homes, and encouraging resilient building practices. These elements contribute to lower utility costs for homeowners and a reduced environmental footprint, aligning with broader national goals.

In conclusion, the 2026 federal housing initiatives are crafted with an eye towards enduring benefits. By promoting sustainable homeownership, these programs aim to empower families to build lasting wealth, contribute to thriving communities, and secure their financial futures for years to come. This forward-thinking approach is a cornerstone of the new policy framework.

| Key Initiative | Brief Description |

|---|---|

| Down Payment Assistance | Grants and loans to reduce initial out-of-pocket costs for homebuyers. |

| Interest Rate Subsidies | Programs designed to lower effective mortgage interest rates for eligible borrowers. |

| Tax Credits | New or expanded tax benefits to offset various homeownership expenses. |

| Streamlined Refinancing | Simplified processes for existing homeowners to reduce their mortgage payments. |

Frequently Asked Questions About 2026 Housing Initiatives

Eligibility is expected to primarily target low-to-moderate income families and first-time homebuyers. Specific income thresholds will vary by region, and other factors like credit score and participation in homebuyer education may also apply. Detailed criteria will be released closer to 2026.

The 10% savings can come from a combination of factors, including reduced interest rates through subsidies, down payment assistance lowering the principal loan amount, elimination of Private Mortgage Insurance (PMI), and new or expanded tax credits for homeowners. These benefits collectively reduce both upfront and ongoing costs.

While the general framework is becoming clear, the precise details, including specific eligibility requirements and application procedures, are anticipated to be fully announced in late 2025 or early 2026. Interested families should monitor official government housing agency websites for updates.

Families should focus on improving their credit scores, saving for a down payment, and researching local housing markets. Attending homebuyer education courses and consulting with financial advisors can also provide a significant advantage in preparing for the application process.

While many programs target first-time homebuyers, some initiatives, such as streamlined refinancing options and expanded tax credits, are expected to benefit existing homeowners. It’s advisable for all homeowners to review the specific programs as details become available to identify potential savings opportunities.

Conclusion

The upcoming new federal housing initiatives for 2026 represent a monumental effort to reshape the landscape of homeownership in the United States. With the potential to save families up to 10% on mortgage costs, these programs are poised to offer unprecedented financial relief and open doors for countless individuals and families. By understanding the core components, preparing proactively, and staying informed, aspiring and current homeowners can position themselves to fully leverage these significant opportunities. The promise of more affordable and sustainable housing is a welcome development, signaling a brighter future for American families and the broader economy.