Estate Planning in 2026: Updated Federal Gift and Estate Tax Exemptions You Need to Know.

As we approach 2026, the landscape of estate planning is poised for significant transformation. The federal gift and estate tax exemptions, which have been at historically high levels, are scheduled to revert to their pre-2018 amounts, adjusted for inflation. This impending change presents both challenges and opportunities for individuals and families seeking to protect their wealth and ensure a smooth transfer of assets to future generations. Understanding these critical adjustments and their implications is paramount for effective estate planning. This comprehensive guide will delve into the specifics of the Estate Tax Exemptions 2026, offering insights into what to expect and outlining proactive strategies to safeguard your legacy.

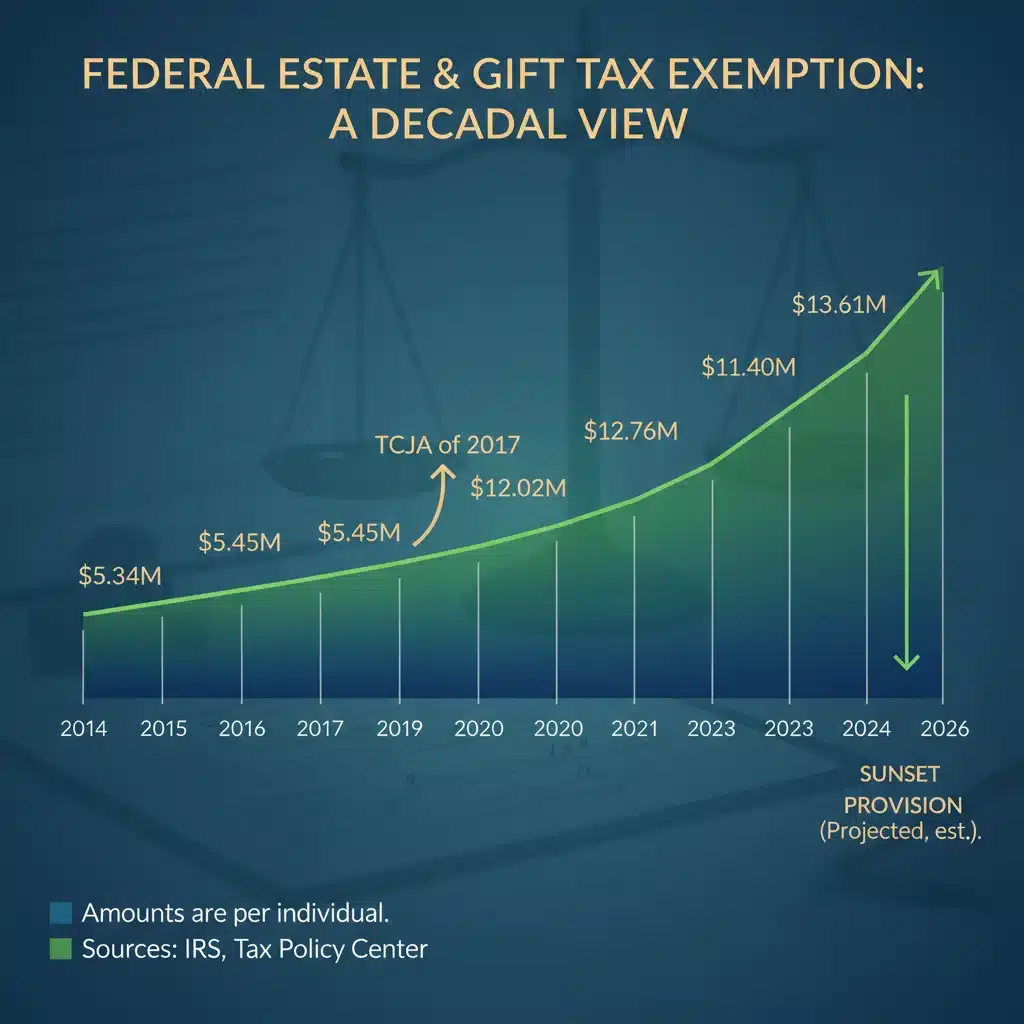

The Current Landscape: A Look Back at the TCJA

To fully grasp the magnitude of the upcoming changes, it’s essential to understand the Tax Cuts and Jobs Act (TCJA) of 2017. This landmark legislation dramatically increased the federal estate and gift tax exemption amounts. For individuals, the exemption nearly doubled, reaching an inflation-adjusted figure of $11.18 million per individual in 2018, and climbing to $12.92 million in 2023 and $13.61 million in 2024. For a married couple, this meant the ability to pass on over $27 million free from federal estate and gift taxes. This unprecedented generosity provided a significant window of opportunity for high-net-worth individuals to engage in sophisticated estate planning strategies, such as gifting substantial assets during their lifetime, without incurring gift tax.

The TCJA provisions, however, were not permanent. They were designed with a sunset clause, meaning they are set to expire on December 31, 2025. This expiration will trigger a return to the exemption levels that existed prior to the TCJA, adjusted for inflation. This scheduled reversion is the primary driver behind the urgent need for individuals to re-evaluate their estate plans in anticipation of the Estate Tax Exemptions 2026.

Understanding the Sunset: What Happens in 2026?

When the TCJA provisions sunset, the federal estate and gift tax exemption amount is projected to revert to approximately $7 million per individual, adjusted for inflation from the 2011 baseline of $5 million. While the exact figure will depend on inflation rates leading up to 2026, it represents a substantial reduction from the current exemption. This means that estates previously exempt from federal estate tax may find themselves subject to it, and individuals who made large gifts under the higher exemption amounts may need to consider the implications if they continue to make large gifts after 2025.

It’s crucial to understand that the federal estate tax is levied on the transfer of a deceased person’s taxable estate, which includes everything the individual owned or had certain interests in at the date of death. The federal gift tax applies to transfers of property by gift during a person’s lifetime. Both taxes share a unified credit, meaning the lifetime exemption applies to both gifts made during life and assets transferred at death. The scheduled decrease in the exemption will directly impact the amount of wealth that can be transferred tax-free, making proactive planning for the Estate Tax Exemptions 2026 more critical than ever.

Who Will Be Affected by the 2026 Changes?

The impact of the 2026 changes will primarily be felt by individuals and couples with significant wealth. While the current high exemption levels have provided a comfort zone for many, the reduction will bring more estates into the taxable threshold. Even those who previously thought their estates were well below the exemption might find themselves subject to federal estate tax if they haven’t planned accordingly. This includes:

- High-Net-Worth Individuals: Those with estates currently valued between the projected 2026 exemption and the current exemption will be most directly impacted.

- Business Owners: The value of a business can significantly contribute to an individual’s overall estate, making proper succession planning and valuation crucial.

- Families with Appreciating Assets: Real estate, stocks, and other investments that have appreciated significantly over time can push an estate’s value into taxable territory.

- Individuals with Large Life Insurance Policies: While life insurance proceeds often pass income tax-free, they are generally included in the gross estate for estate tax purposes if the insured owned the policy.

It’s important to remember that state estate or inheritance taxes may also apply, and these often have much lower exemption thresholds than the federal tax. Therefore, even if your estate remains below the federal threshold, state-level taxes could still be a concern.

Key Strategies for Navigating the 2026 Changes

Given the impending reduction in the Estate Tax Exemptions 2026, now is the opportune time to review and potentially revise your estate plan. Here are several key strategies to consider:

1. Maximize Lifetime Gifting Before 2026

One of the most effective strategies to utilize the higher exemption amounts is to make substantial gifts before the end of 2025. The IRS has confirmed that there will be no ‘clawback’ for gifts made under the higher exemption amounts. This means that if you make a gift that uses part of your $13.61 million exemption in 2024 (or $12.92 million in 2023), and the exemption amount drops to $7 million in 2026, the gifts made under the higher exemption will not be retroactively taxed. This ‘use it or lose it’ scenario makes lifetime gifting a powerful tool. Consider gifting assets that are expected to appreciate in value, as this not only removes the current value from your estate but also any future appreciation.

- Direct Gifts: You can directly gift assets to individuals, utilizing your lifetime exemption.

- Trusts: Establishing irrevocable trusts, such as Spousal Lifetime Access Trusts (SLATs) or Grantor Retained Annuity Trusts (GRATs), can be excellent vehicles for making large gifts while potentially retaining some indirect benefit or control for the grantor.

- Annual Exclusion Gifts: Don’t forget the annual gift tax exclusion, which allows you to give a certain amount (currently $18,000 per recipient per year in 2024) to as many individuals as you wish without using any of your lifetime exemption.

2. Review and Update Your Existing Estate Plan

If you already have an estate plan in place, it’s critical to review it with your estate planning attorney and financial advisor. Your current plan may have been drafted under different tax laws, and the 2026 changes could render some provisions less effective or even counterproductive. Pay close attention to:

- Formula Clauses: Many wills and trusts contain formula clauses that distribute assets based on the federal estate tax exemption amount. These clauses need to be re-evaluated to ensure they align with your intentions under the lower exemption.

- Beneficiary Designations: Ensure your beneficiary designations for retirement accounts, life insurance policies, and other assets are up-to-date and reflect your wishes in light of potential tax implications.

- Marital Deduction Planning: For married couples, revisit strategies involving the unlimited marital deduction to ensure optimal tax efficiency.

3. Consider Advanced Estate Planning Techniques

For those with very large estates, more sophisticated techniques may be necessary to mitigate the impact of reduced exemptions. These include:

- Irrevocable Life Insurance Trusts (ILITs): An ILIT can hold a life insurance policy, removing the death benefit from your taxable estate. This can provide liquidity to your heirs to pay estate taxes without those funds being subject to estate tax themselves.

- Grantor Retained Annuity Trusts (GRATs): This strategy allows you to transfer appreciating assets out of your estate with minimal or no gift tax consequences. You retain an annuity payment for a term of years, and any appreciation above the IRS hurdle rate passes to your beneficiaries tax-free.

- Charitable Planning: Charitable trusts, such as Charitable Remainder Trusts (CRTs) and Charitable Lead Trusts (CLTs), can reduce your taxable estate while fulfilling philanthropic goals.

- Family Limited Partnerships (FLPs) and Limited Liability Companies (LLCs): These entities can be used to transfer assets to younger generations at a discounted value, as ownership interests in FLPs/LLCs are often subject to valuation discounts for lack of marketability and control.

4. Understand Portability

Portability allows the surviving spouse to use any unused portion of the deceased spouse’s federal estate tax exemption. This means that a married couple can effectively combine their exemptions. While portability is a valuable tool, it’s essential to understand its limitations and ensure that your estate plan is structured to take full advantage of it. For instance, portability must be elected on a timely filed estate tax return (Form 706) for the deceased spouse’s estate, even if no tax is due. This election is vital for maximizing the combined exemption, especially with the impending reduction in the base exemption amount for Estate Tax Exemptions 2026.

5. Revisit Asset Ownership and Titling

How your assets are owned can have significant estate tax implications. Reviewing the titling of your assets, such as real estate, bank accounts, and investment portfolios, is a crucial step. Joint ownership with rights of survivorship, for example, can bypass probate but might not always be the most tax-efficient strategy. Consider whether transferring assets to a trust or changing ownership structures could better align with your estate planning goals and minimize potential estate tax liabilities.

6. Engage in Open Communication with Your Family

Estate planning is not just about taxes; it’s also about ensuring your wishes are carried out and minimizing potential family disputes. Openly discussing your estate plan with your loved ones can help them understand your intentions and prepare for what’s to come, especially as tax laws evolve. This communication can also help identify any concerns or misunderstandings that can be addressed proactively.

The Role of Professional Advice

Navigating the complexities of federal gift and estate tax laws, especially with the upcoming changes in Estate Tax Exemptions 2026, requires expert guidance. An experienced team of professionals, including an estate planning attorney, financial advisor, and tax accountant, can provide tailored advice based on your unique financial situation and goals. They can help you:

- Assess Your Current Estate: A thorough review of your assets, liabilities, and existing estate documents.

- Project Future Tax Liabilities: Estimate potential estate and gift tax liabilities under the new exemption amounts.

- Develop a Customized Plan: Create a strategic plan that utilizes available exemptions and minimizes tax exposure.

- Implement Planning Techniques: Assist in the proper execution of trusts, gifts, and other advanced strategies.

- Stay Informed: Keep you updated on any legislative changes or new interpretations of tax law that could impact your plan.

Potential for Legislative Changes

While the sunset of the TCJA provisions is currently scheduled, it’s important to acknowledge that Congress could theoretically intervene before 2026. However, relying on potential legislative changes is not a sound planning strategy. It’s always best to plan based on current law and the scheduled sunset. If new legislation is passed that alters the Estate Tax Exemptions 2026, your professional advisors can then help you adjust your plan accordingly. The current political climate and economic conditions make it difficult to predict the exact nature of any future tax legislation, reinforcing the need for proactive planning under the existing framework.

The Interplay with State Estate and Inheritance Taxes

While the focus of this article is on federal estate and gift tax exemptions, it’s crucial not to overlook state-level taxes. Several states impose their own estate tax, inheritance tax, or both. These state taxes often have much lower exemption thresholds than the federal government, meaning an estate might be exempt federally but still subject to state tax. Some states also do not have portability provisions, which can complicate planning for married couples. As you plan for the federal Estate Tax Exemptions 2026, be sure to consult with your advisors about the specific estate and inheritance tax laws in your state of residence, as these can significantly impact your overall tax liability.

For example, states like New York, Illinois, and Oregon have estate taxes with exemptions far below the current federal level. Maryland and New Jersey have inheritance taxes, which are levied on the beneficiaries receiving the assets, rather than on the estate itself. Understanding these nuances is vital for a truly comprehensive estate plan.

The Importance of Timing: Why Act Now?

The window of opportunity to take advantage of the historically high federal gift and estate tax exemptions is closing rapidly. With the sunset provision taking effect on January 1, 2026, individuals have a limited time to implement strategies that utilize these higher exemption amounts. Waiting until the last minute can lead to rushed decisions, potential errors, and missed opportunities. Proactive planning allows for a thoughtful, well-executed strategy that maximizes tax efficiency and aligns with your long-term legacy goals. The complexity of some advanced planning techniques means they can take time to establish and fund properly, reinforcing the urgency of acting sooner rather than later to capitalize on the current Estate Tax Exemptions 2026 opportunities.

Furthermore, the value of assets can fluctuate. Gifting assets while their value is high (but still within the current exemption) can remove that value, and all future appreciation, from your taxable estate. Conversely, holding onto assets that decline in value before gifting could lead to less effective use of your exemption. A well-timed strategy is key.

Case Study: Illustrating the Impact of Exemption Changes

Consider a hypothetical couple, the Smiths, with a combined estate valued at $20 million. Under the current (2024) federal exemption of $13.61 million per individual, their combined exemption is $27.22 million, meaning their entire estate would pass free of federal estate tax. However, if they do not take action and the exemption reverts to approximately $7 million per individual in 2026, their combined exemption would be around $14 million. This would leave $6 million of their estate ($20 million – $14 million) potentially subject to federal estate tax, which is currently at a rate of 40%. This could result in a federal estate tax liability of $2.4 million.

If, prior to 2026, the Smiths had gifted $6 million of appreciating assets into an irrevocable trust for their children, they would have utilized a portion of their current higher exemption. This would remove those assets, and their future appreciation, from their taxable estate. Upon the exemption reduction in 2026, their remaining estate would be $14 million, falling within the projected combined exemption, thus avoiding federal estate tax entirely. This simple illustration underscores the significant financial impact of proactive planning concerning the Estate Tax Exemptions 2026.

Conclusion: Secure Your Legacy by Acting Now

The impending changes to the federal gift and estate tax exemptions in 2026 represent a critical juncture for estate planning. While the reduction in exemption amounts will undoubtedly impact many high-net-worth individuals, it also provides a clear call to action. By understanding the implications of these changes and implementing proactive strategies such as maximizing lifetime gifting, reviewing existing plans, and considering advanced techniques, you can effectively mitigate potential tax liabilities and ensure your legacy is preserved according to your wishes. Engaging with experienced estate planning professionals is not just advisable; it’s essential to navigate this evolving landscape successfully. Don’t wait until 2026 to address these crucial matters; the time to plan for the future of your wealth is now.